Is your house an asset or a liability

Your house is a liability, your house is a liability.

You might have heard this from many people. There are many kinds of people who say this, but i have divided it into two categories.

1. The New Financial Literates.

These are the kind of people who have finished reading a book like “Rich Dad Poor Dad” , and suddenly becomes financial experts and take the quotes from the book “House is a Liability”. But, do you really know what is the business the author is doing. He is into Real Estate. He owns more than 3500 properties. Yeah, you heard it right , he owns more than 3500 liabilities. Now, comes the second type of people.

The video is from Ultra Legends Club channel which explains everything, so if you want to watch instead of reading check it out:

2. The Loan Phobia guys.

These are the people who will say that you don’t own a home, you own a so much loan, you will hate yourself for rest of your life. Loan is a trap , its a monster , bla bla bla. But, do you know how much debt is in Reliance Industries , the company of Richest person in India. It has a debt of 1,54,478 crores as on 2019, at the time of writing this article. Yeah, you heard that right. Having a debt for starting something or for owning an asset which will put money in your pockets later, is really not such a bad idea.

There is one more kind of people, my favourite kind and because of whom , i have decided to write this blog, those who say that

Renting is cheaper than owning.

Now, let us run some numbers and see if that is really true. I have two properties, one of which i believe is an asset , and other one is neither a liability , nor an asset. Let us crunch some numbers and see whether it is really an asset or a liability.

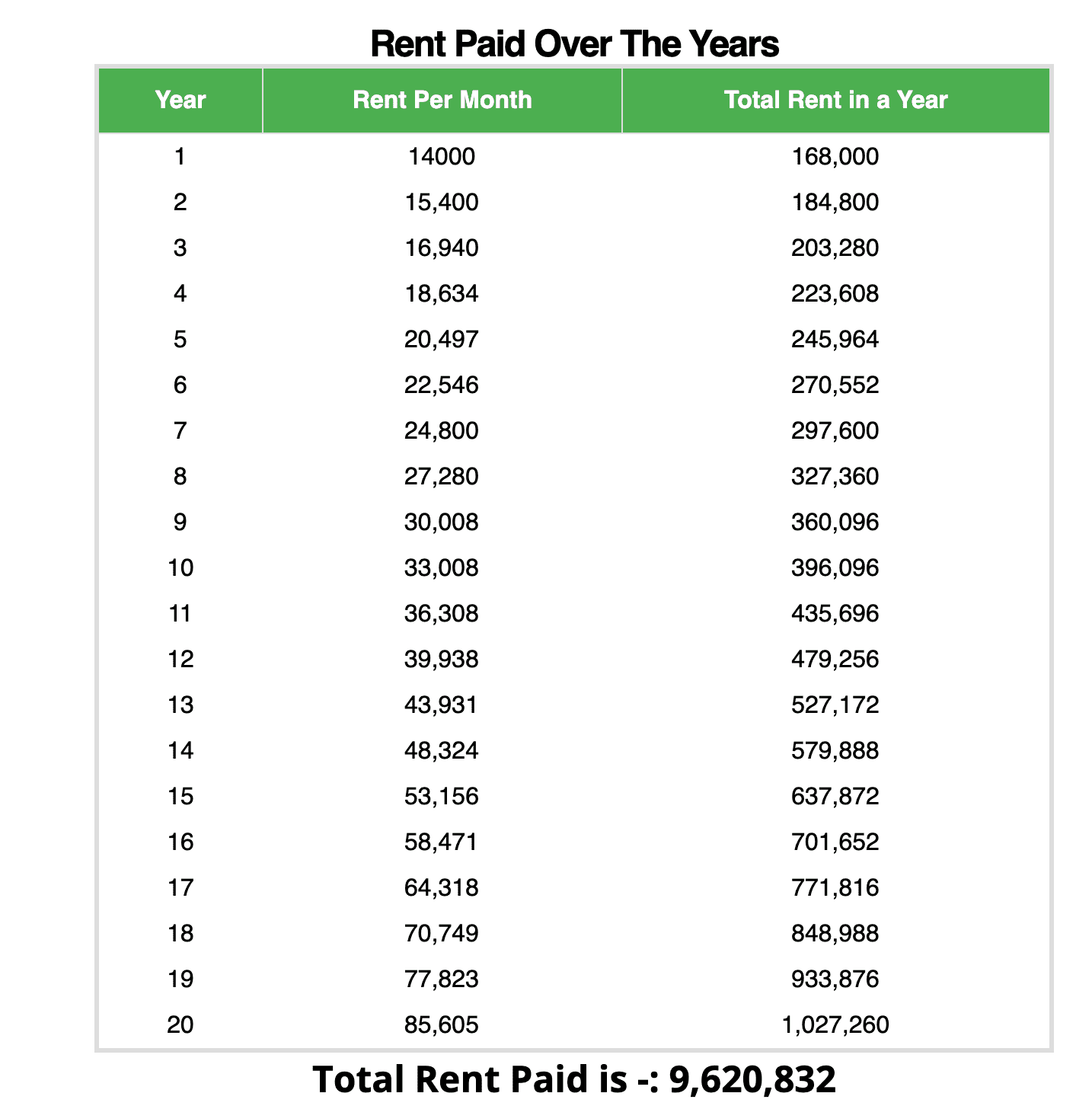

Now i bought a small full furnished 2 BHK house for 31 lakhs. After making a downpayment, and loan of 20 years, the monthly EMI comes at around 24k per month at current rate of interest. I get rent of around 14k per month by renting it out.

I live in bangalore, and here rent increases by around 10% every 11 months , because every 11 months the rental agreement gets renewed. Now for the sake of calculation, lets assume , it gets renewed every year i.e in 12 months. You can check the rent calculator from here Rent Calculator

Now, lets dig into the conclusions

- The EMI which is i am paying will remain almost the same, however the rent which will be asked will increase by 10% every year.

- After 7 years , the rent which i receive will be greater than the EMI which i will be paying.

- For the calculations perspective i have assumed 20 years , but even after finishing my loan , still i will be getting rent each year.

Apart from these things, there are also few other factors to consider

- I will also get the tax benefits on the interest amount which i pay , as well as on the principal amount.

- If after 20 years i want to sell the apartment, i will be able to pay that for much appreciated value

- If the inflation is more the money which you borrowed from the bank at lower interest become more cheap , or deprecates in value, but the rents on the other hand increases as inflation increases.

Yeah, yeah but what about the other things. There are always other things

- Maintenance After the tenant has moved in, he/she is responsible for maintaing the property. In my stay in rental properties, i have not seen any lanlord paying the maintenance after tenant has moved.

- Cool Off Period The tenant has to give you a notice of 1 month, this time is more than enough to find new tenants.

- Damages If there is any kind of damage to the property , that amount will be deducted from the Deposit

Still, if you think a house is a liability , then think again.

Is a rental property always a good option, or is any kind of investment in real estate always good. No, it is not. To be fair enough, lets look at the downside of owning a property

- If you want to start your own business at some point of time, after few years , then investing in property will not be a good option, because in the initial years , the money will go out of your pocket, cash flow will be outwards. It will be difficult to start something with EMIs going on.

- You need a high amount for downpayment.

- It is not as liquid as stocks, since it is not possible to sell it anytime whenever you want to.